Natural Gas as fuel source for navy industry

When in 2006 Dr Jorge Antunes started teaching at Newcastle University in England, propulsion systems for gas engines, most of his colleagues thought the idea too advanced for the time, not to say misplaced. For many, Natural Gas would never be seen as a marine fuel. Until then, Natural Gas was used mainly in Japan and Norway on board some local traffic vessels, such as Glutra, a small RO-RO of 100 passengers, as shown in figure 1 and whose main characteristics are indicated in table 1.

Figure 1 – The “Glutra” Norway (2000)

Table 1 – Main data of RO-RO “Glutra” (2000)

| Main Dimensions | |

|---|---|

| Length (m) | 94.80 |

| Mouth (m) | 15.70 |

| Draft (m) | 5.15 |

| Service Speed (Knots) | 12 |

| Displacement (ton) | 640 |

| Capabilities | |

| Private Cars | 100 |

| Passengers | 300 |

| Propeller Installation | |

| 4 Mitsubishi GS12R-PTK, 12 Cylinders in V | 675 kW / unit |

| LNG Capacity | |

| AGA CRYO | 2 x 32 m3 |

| Propellers | |

| 2 columns Schottle STP 1010 | 1000 kW |

In 2000, there were only eight vessels using natural gas as the main fuel, mainly inland waterways dedicated to the transportation of passengers and tourism. The Natural Gas was at that time taking the first steps, and the expectation of becoming the “fuel for the navy”, although small, would be forced by various means to become the “intended fuel”.

In this article, we will briefly and simply address the underlying problem of natural gas as a fuel for the navy, which, necessarily, is such a complex matter that cannot be satisfactorily scaled in a magazine article.

What is Natural Gas?

Natural gas is a mixture of hydrocarbons (ones lighter and others heavier), which burning is believed to be “environmentally friendly”.In other words, burning is cleaner than other conventional hydrocarbons such as gasoline, diesel, heavy fuel, etc. Natural gas is a hydrocarbon, which means that it consists of carbon and hydrogen. The simplest hydrocarbon is methane; which contains one carbon atom and four hydrogen atoms. Natural gas can be found by itself or in association with oil. It is colourless and odourless although it is a mixture of hydrocarbons. Besides being mainly constituted by methane, it can comprise other hydrocarbons such as ethane, propane, butane and water, oil, sulfur, carbon dioxide, nitrogen, and other impurities mixed with the gas when it leaves the ground. These impurities are removed before natural gas is delivered to final consumers. The fact that natural gas is fuel and its burning is cleaner than other types helps to strengthen its position as one of the most commonly used fuels.

Natural gas is measured in many units, although the most common unit of measurement is the Gigajoule (GJ), the metric measure for heat or energy. Other forms of measurement used in the natural gas industry are MCF (Thousand Cubic Feet) and Btu (British Thermal Unit). Natural gas is found in reservoirs below the surface of the earth. Large layers of dome rock trap the natural gas beneath the surface. Once removed from its underground reservoir, the natural gas is transferred to processing facilities to remove impurities and other by-products. Some of these by-products, including ethane, propane, butane, and sulfur, are extracted for other uses.

After being processed, clean natural gas (almost pure methane) enters through pipelines in the liquefaction and storage facility, followed by a cryogenic pipeline to be loaded in a ship that delivers it to another terminal where it is vaporized for mains power of gas pipelines. On the other hand, another part is dispatched in a liquid tanker to power the so-called UAGs- Autonomous Gas Units, that feed smaller gas networks in remote locations for which the use of pipelines is not economically viable. We are therefore talking about a process, which requires the cleaning of the gas, its liquefaction (in this process volume is saved, namely 584 m3 of gas in the gaseous state under PTN conditions, are reduced to 1 m3). For convenience to the reader, one can say that, 1m3 LNG = 584 m3 GN @ PTN = 0.405 MT LNG = 6173 kWh = 22.19 GJ = 21.04 MBTU.

The production chain of Natural Gas and the environment

The energy required to liquefy 1kg of gas in the gaseous state is about 1188 kJ or 1188 kJ / kg of LNG. (Finn et al., 1999). Although in practice the calorific value of the gas may vary with its origin, as well as with the liquefaction technology in the process, about 8% of the energy contained in a kilogram of natural gas is lost in its liquefaction process (Patel, 2005). By itself, it significantly increases the carbon footprint. This does not include all processes upstream and downstream of the liquefaction process.

The natural gas market

About 10 years ago Europe believed that a golden age of natural gas was near, leading many investors and market analysts to blindly believe in something that did not happen, quite the opposite. Investing heavily in infrastructures, some megalomaniacs, easily accepted that consumers would naturally occur as soon as those structures were ready to operate.

It turns out that 10 years later, the size of the natural gas market is no more than one-fifth of what was expected, noting that the natural gas supply chain has room for more “players” essentially characterized by their small size. Given the above circumstances, the increase in natural gas consumption is therefore urgent, and although natural gas is not a natural fuel for the navy, the navy serves the purpose given its considerable energy consumption. The natural gas market for the navy is still to be developed, examples that have occurred are timid, usually with very particular operational characteristics in terms of geographic areas, highly subsidized, and essentially limited to few types of ships. The most frequent types of ships are offshore support vessels, some cargo ships, and RO-ROs.

As it is known, there are emission control areas (ECA’s), which objective is mitigate the effect of emissions produced by maritime activity along the coasts of some countries, notably above the Channel, the entire Baltic Sea, including part of the west coast of Norway, as well as the entire coast of the United States.

Other ECA zones are being declared or soon to be. It is known that the Camara Municipal de Lisboa, recently voted (with a single abstention the definition of an ECA zone for Lisbon and the mainland coast of Portugal). Annex VI is relatively recent within the MARPOL Convention and is essentially aimed at controlling the emissions of ships, such as CO2 and NOx, among others, and consequently rationalizing the use of energy in maritime activity. It is widely accepted that poor energy use leads to more significant CO2 emissions but also to other pollutants, such as particulate matter, NOx, and VOCs.

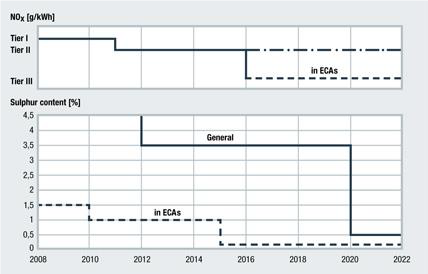

Figure 2 – Timescale of implementation according to MARPOL 73/78 Annex VI for the emission limits of SOx and NOx (Source MAN – IMO MARPOL)

Although emissions of air pollutants are covered by the MARPOL VI Convention, only NOx emissions have limit values. In the case of SOx, the limit was imposed on the maximum permissible sulphur content in fuels, which since 2015 has been reduced to 0.1%. From 2020 this limit will be 0.5% for non-ECA areas as shown in figure 2. With regard to the CO2 value, the European Union (which has decided to go ahead with the IMO) is in the process of implementing a mechanism similar to the one used in the land and aviation industry, subject to the MRV (Monitoring Reporting & Verification) mechanism or a market for carbon quotas applied to Shipping. This will certainly catalyze the energy efficiency of vessels. Relatively to the PM10 and PM 2.5 particles, there is still nothing to limit them.

Due to the implementation of tighter legislation on the limitation of gaseous emissions (including aerosols), health expenditure directly linked to air pollution in Europe has been decreasing. Having been worth € 803 billion in 2000, it is expected to be € 573 billion in 2020. Although emissions from land-based sources are decreasing, ship emissions of air pollutants are expected to increase by 5% in 2020, as a result of increased traffic in the northern hemisphere. Europe due to the contribution of pollutant emissions from Shipping alone should increase from 7% in 2000 (or € 58.4 billion) to 12% in 2020, reaching a value of around € 64.1 billion. In Denmark, which is particularly affected by the heavy traffic of ships along its coast, between the Baltic Sea and the North Sea, the reduction of the sulphur content and its SOx oxides should result in a decrease in the health costs of € 627 million in 2000 to the expected € 375 million in 2020. It is with regard to emissions of Nitrogen oxides and sulfur oxides and in particular the emission of particles that natural gas has a notorious advantage on most other fuels notably on HFO (Heavy Fuel Oil) and MDO (Marine Diesel Oil) although the emissions due to the methanol burning are even cleaner. However, this advantage may not be so obvious when comparing carbon footprints, as well as taking account of fugitive gas emissions and the so-called gas slip, in particular when four-stroke engines are used, which by their cycles are characterized by greater or lesser time of valve crossings, leading to the passage of unburnt or semi-oxidized gas, directly to the evacuation system and later emitted into the atmosphere.

Another “Driver” has to do with the strength of the natural gas market, to achieve greater consumption. As already mentioned, existing large infrastructures rapidly need consumers in order to justify themselves economically. It should be noted that some of these gas suppliers are owned by the governments of some countries, such as Norway, where there are the largest number of gas-powered vessels, and where many of the recent projects have received strong support from the There is therefore a strong government and technological strategy action by the Norwegian government. It should also be noted that a large proportion of all ships converted to gas operate in well-defined geographical areas, where supply logistics are assured, as well as the regular consumption of a certain amount of gas.

The “anti-drivers” of gas as fuel for the navy

As mentioned above, there are some “blind knots” that need to be “untied” so that the natural gas can penetrate as fuel for the navy. The first obstacle to natural gas penetration is due to the total lack of definition of long-term gas prices given the fact that the price of gas is heavily influenced by political and strategic interests. However, it is expected that the gas will be offered to the market at a price, which should be around the price of HFO 180 cSt @ 50ºC. That is, it will be a cheaper fuel than the MDO, but its cost should be around that of the HFO operation, that is, it does not bring any economic advantage to the shipowner, who will have to bear the cost of converting his ships plus one supply logistics, as well as crew training.

The price of conversions, typically the conversion of a ship to the main machine of about 5,000 kW is around € 7 million, not including the conversion of its generators and boilers. Loss of cargo space to receive liquid gas tanks, this is when the market for most freight is subject to lowering their values. The supply time and the respective safety zones on the wharf around the vessel to be supplied constitute in itself a difficulty. This is a point to bear in mind, given that LNG bunker operations using conventional means from tanker trucks are very time-consuming, forcing tanker trains to enter ports even to supply small-size cargo ships. They oblige the delimitation of considerable safety zones within the ports, which will entail restrictions on the movement of people and vehicles and consequently on the operation of the ship and the port.

Lack of means for supplying gas bunkers to ships and in particular for a duration close to that used by conventional gas carriers. Also anti-drivers are those projects that may appear less well studied and therefore may lead to poor results, pinching the potential of gas as fuel, as is the case of the application to vessels that receive their benches in liquid gas and which due to their operation have periods of shutdown, such as tugboats, which operate a few hours per week. This is a problem, due to the so-called “boil off” resulting from the boiling of the gas inside their tanks. The boil-off gas will have to be consumed or released in order to maintain the pressure in the cryogenic tank within acceptable values, typically 8 bar. That is, not all ships are suitable candidates to use natural gas, and an unfulfilled project is a bad example for future projects.

Even from the point of view of propulsive (non-electric diesel) installations, namely tugboats or other vessels that operate frequently, it can be said that a propulsion engine, when operated on gas, does not have the same dynamic characteristics as the diesel engine, which can be a problematic obstacle if not fatal. The technical rules of the ports are still to be defined and many times to be harmonized, creating a confusion of procedures difficult to manage, on the part of the crews. No means of combating claims envolve gas.

Emissions from the combustion of natural gas.

The real advantage of natural gas, not being able to assert its economic advantage at least for now, is effectively a more “friendly” burning to the environment. When used as a fuel in 4-stroke engines, and not with a gas slip or other fugitive leaks, emissions are much lower than those resulting from the diesel engine, in terms of NOx, SOx, and Particles, but already in terms of VOCs (Volatile Organic Compounds). The same can not be said, which may lead to the need for the use of a catalytic oxidizer, for slip and VOCs. However, if the same natural gas serves as a fuel for a two-stroke crosshead engine, the advantage is already reduced to particulates and SOx, since NOx and VOCs emissions levels are always above the emission limit values, thus forcing the installation of a tail end gas treatment system such as oxidizing catalysts.

There are in Portugal some interesting projects already in the phase of implementation of others in the draft phase. The Sines-Lisboa-Madeira “Virtual Pipeline” carried out by Gaslink Gas Natural S.A. of Madeira. It is itself an innovative project, based on the transport by road and ship of cryogenic containers loaded of LNG, that feed a UAG (Autonomous Gas Unit) which in turns provides groups of electrical production with Dual Fuel motors. The capacity is limited to the number of containers that can be transported per unit time, thus depends on the availability of sea transport which has a carbon footprint originated by the considerable transport. Logistical problems are not particularly problematic due to the fact that containers are shipped as dangerous cargo, and not as fuel. Investment is relative, and the technologies involved well-known, having an anchor client in Madeira.

In the pre-project stage is the Trafaria terminal which belongs to OZ Energia S.A. It can be a complete response to the needs of the port of Lisbon and other contiguous ones.

Figure 3 – View of the north side of the Tagus river from the OZ Energia terminal in Trafaria

The terminal, whose capacity can reach 30,000 m3, will have a pontoon (Getty) with the capacity to receive LNG and export and supply ships with all safety conditions. The project of OZ Energia S.A. will have all the security conditions necessary for the supply of bunkers to ships, but it is still planned within the scope of this project the existence of an LNG bunker vessel.

In the port of Sines, although there is LNG, it is necessary to design and build a terminal dedicated to the supply of LNG to vessels that arrive at that port, whose main customers in the future will be cargo-containers, because they are the ones that most navigate in ECA zones, distributing containerized cargo (not limited to) the countries where ECA zones are already implemented. There are other operators in particular from Spain, who are profiling themselves as gas suppliers by tanker truck.

Conclusions

Natural gas as a fuel for the navy is still in its early stages, sometimes with successes, others with technical failures. It has become the ” fashionable non-fuel option” although there are others like methanol that compete with it. Some of the most frequent problems were presented, being absolutely necessary the time for the development and clarification of all the participants. This is a time that requires big investments, time, technology and necessarily money. One thing is sure, natural gas will be one of the main fuels for the navy, notwithstanding the political and strategic pressure exerted on it, as well as the holders of large (terminal) facilities and means of transport. Natural gas as fuel presents major challenges for shipping, the main one at the moment is the lack of definition of its cost to the navy, followed by its geographic availability and necessary technology. Another challenge would be the price of the conversion of the main machines to operate with natural gas.

Natural gas competes with other fuels, in particular when associated with exhaust gas treatment technologies, such as scrubbers or oxidative catalysts. As for the emissions of natural gas and its carbon footprint, it can be said that the numbers need to be well looked at, but their local effect is less aggressive than the burning of other conventional fuels, particularly when they are used without gas treatments.